July 19, 2026

12 min read

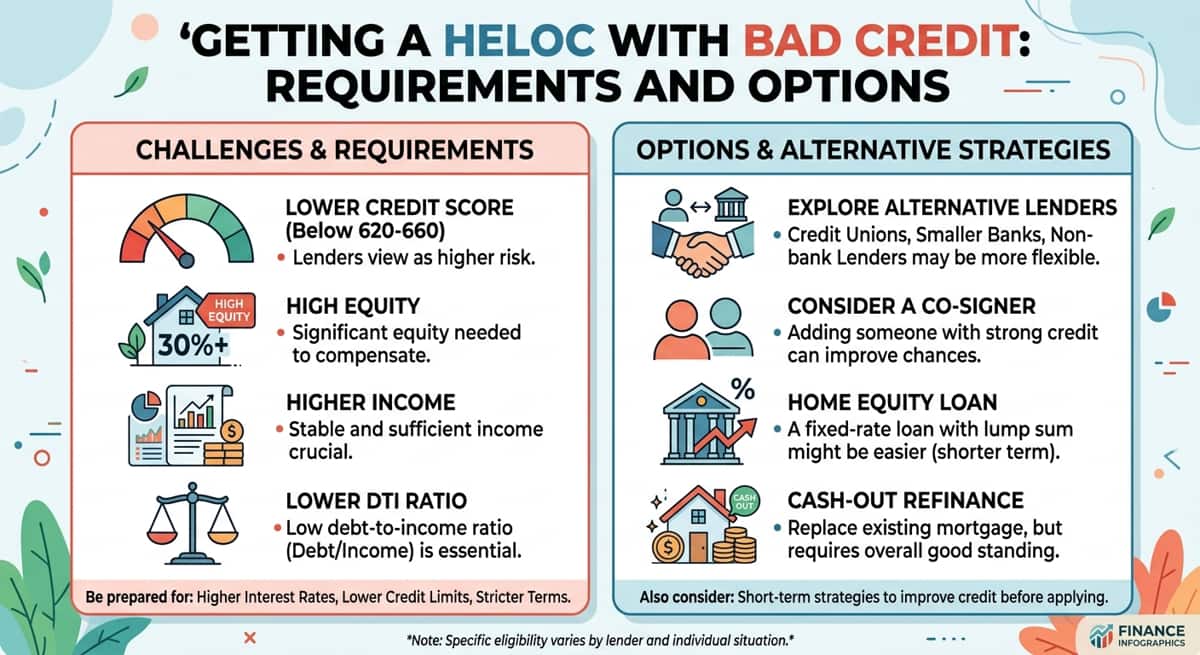

HELOC

How Soon Can You Get a HELOC After Buying a House?

Most lenders require waiting 6 to 12 months after buying a home to get a HELOC. This "seasoning period" ensures stable home value and reliable mortgage payments. To qualify sooner, you need strong credit, low debt-to-income, and at least 15–20% built-in equity from a large down payment.